May 24, 2010

Weekly percentage performance for the major indices

Based on last Friday’s official settlement...

INDU: -4.0%

SPX: -4.2%

COMPQ: -5.0%

RUT: -6.4%

Economy

The Leading Economic Indicators came in at -0.1% versus consensus of 0.2%. Nondefense capital goods orders were up, while the pace of deliveries and building permits were the largest negative contributors to the decline in LEI.

Money Supply

The chart below, courtesy of the National Inflation Association, shows the growth (red and blue lines) and total (green line) money supply in the US. The growth rate, a 13 week moving average, was an astronomical 100% at the peak of the crisis, and has since pulled back to what appears to be a low double digit rate.

Regardless of how the government tries to cover up inflation (see Inflation below), the end result will be the same. The dollar, and potentially all paper currency, is headed towards Armageddon.

Credit Conditions

The European credit crisis is wreaking havoc on the credit markets. As we showed last week, LIBOR is spiking. Additionally, corporate credit issuance has slowed dramatically and credit spreads are rising, all signs of another brewing credit crisis. Credit-default swaps soared in Europe this week after German Chancellor Angela Merkel implemented a curb on using CDS to speculate on sovereign debt. Rising CDS rates signal investor concern about credit quality.

Spreads on corporate bonds rose to 170bps this week, up from 140bps a month ago. Libor, the rate which banks charge each other for borrowing amongst themselves, rose to the highest level in almost a year to just under 50bps. The LIBOR-OIS spread now sits at 25bps, up from 6bps in March. The rising spread indicates a concern about counterparty risk between lenders. According to Merrill Lynch, the rise in the LIBOR-OIS spread simply signifies reluctance among US banks to lend to European banks.

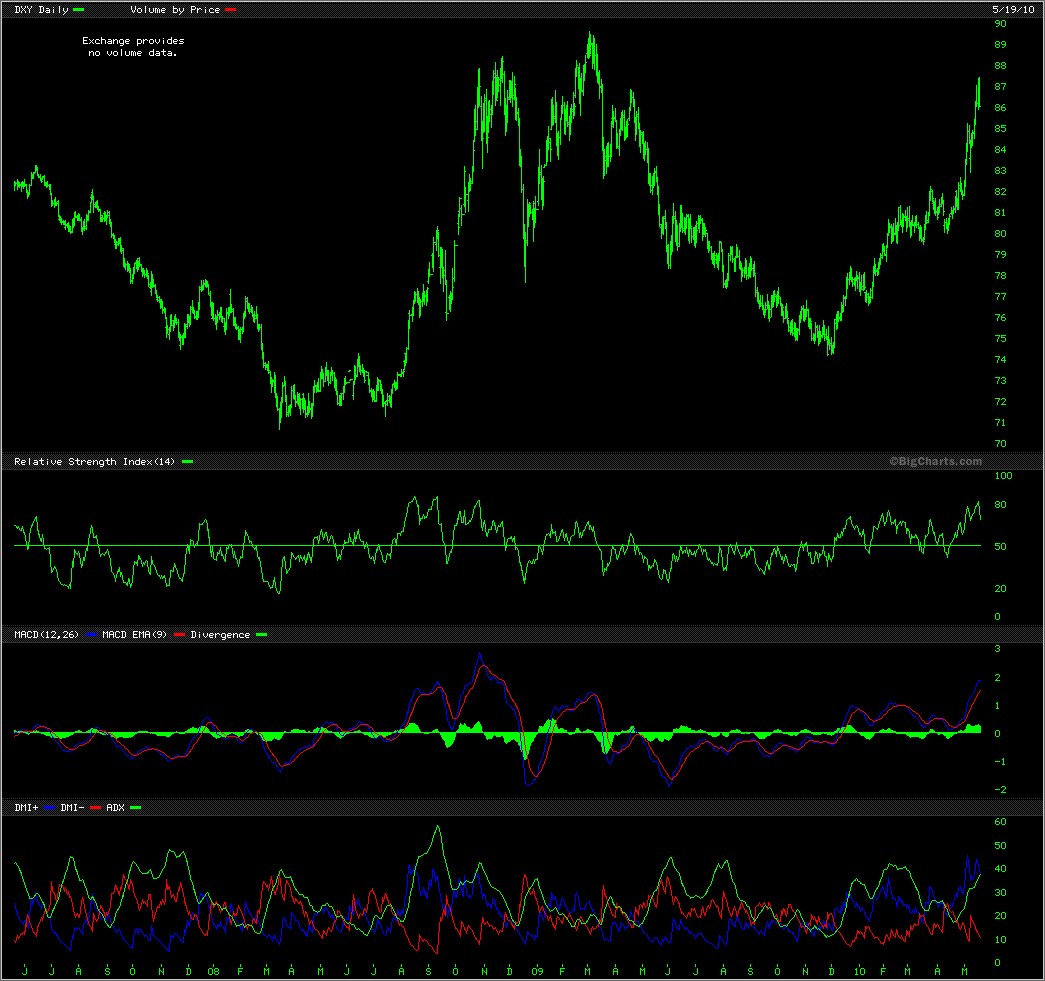

Currency

The dollar has been a beneficiary of the recent problems with the Euro. The chart below, courtesy of reader Bob Rezaee, shows the movement in the dollar since the Euro began experiencing its issues near the end of last year.

Meltup

The National Inflation Association created this video discussing the impact and under-statement of inflation. I think it is well done, although I feel the part which discusses silver is much too long and too much of a propaganda section.

Illinois

We have commented extensively about the problems in California, but it appears that Illinois is in even worse shape than the Golden State. According to the Illinois Comptroller, they haven’t paid close to $4.5 billion in bills so far this year. In January the state issued $3.5 billion in pension bonds to pay the state’s obligations to the retirement system.

Could Illinois and California be the US version of the PIIGS?

Oil

Concerns over demand and oversupply of oil combined with a surging dollar have pushed the price of West Texas Intermediate under $70 per barrel. The chart below, courtesy FINVIZ.com, is a five year chart on the commodity.

Alternative Energy

Construction is slated to begin later this year on a 49-megawatt geothermal-energy plant in the U.S. after financing for the project was finalized last week. The $399 million project is being developed by EnergySource. The company plans to pursue as many as four additional geothermal projects, with the next one possibly ready as early as 2013.

Remember about a year ago we compared all the alternative sources of energy, and geothermal was the most economically attractive.

Inflation

I have written extensively about the hedonistic adjustments made to the CPI measure in 1993. Shadowstats.com produced the chart below showing the official CPI (orange) and their own estimate of CPI without the hedonistic adjustments. According to the National Inflation Association, the underestimation of CPI over the past two decades has resulted in social security beneficiaries receiving approximately 50% of what they would have received had the measure not been altered.

It makes me wonder how reliant Greenspan was on this meausre when he kept rates artificially low during a 10 year period, and also how close to bankruptcy the Social Security program would be without those adjustments?

Real Estate

According to Jim Welsh, Fannie Mae and Freddie Mac have been taken over by the U.S. government, and the taxpayers will have to make good on their combined losses of at least $400 billion. It’s also worth noting that between 1988 and 2007, Fannie and Freddie made almost $200 million in campaign contributions to Congress. The three largest recipients in the Senate were Christopher Dodd, John Kerry, and Barack Obama.

Conclusion

I mentioned last week that 400 point gains on the Dow typically were bad, and the market reacted as expected with a big drop this week. I’ve closed my QID positions (double short NASDAQ). I discussed a correction taking the S&P 500 to the mid-low 1000’s, and while we aren’t quite there yet, I am going to at least stay off the shorts for now. If we get more negative movement in the credit markets, I may go back in on the short side. I have also been adding to my holdings in high quality, more stable large caps with solid dividends.

Have a great week.

Ned

No comments:

Post a Comment