I hope this finds you well.

The first half of 2020 is finally over and it certainly felt

more like a decade than half a year. There was more activity politically,

economically, and in the markets than in any six month period I can remember. It

seems remarkable that a mere three months ago the market hit a new low, accentuated

by a near record decline of 12% in a single day. A mere four months ago we celebrated someone’s

20th birthday in style-that seems like two years ago.

After imploding in the first quarter, the markets staged one

of the great comebacks in market history, rising over 20% in the second quarter

to post one of the best quarters in decades. In spite of record declines in GDP

combined with record spikes in unemployment, the market stands a mere 4% below

where it started the year. There has been some interesting divergence as the

NASDAQ has risen by over 12%, led by large cap technology stocks; the S&P

500 has declined 4%; the Dow Jones has declined 10%; and the MSCI All World Index

has declined 7%. For the first time in

over decade there has been significant divergence in markets as the difference

between winners and losers, which had been minuscule, is now defined by those which

are thriving versus those facing severe stresses to their business. This should

be the perfect environment for active stock management, however, once again managers

are failing to outperform markets. We are early in this process and will monitor

how it progresses.

The craziest economic reports are coming in the employment data.

The change in non-farm payrolls plummeted by 1.3 million in March and a

staggering 20.8 million in April. The

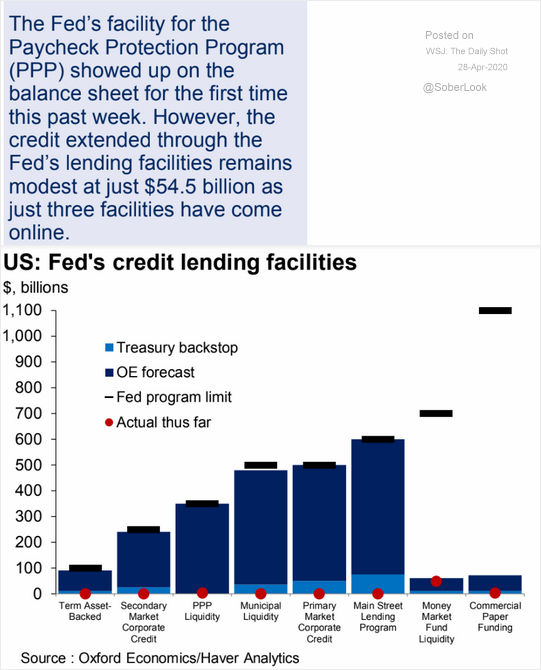

Federal Reserve provided massive monetary stimulus, and the Federal Government

provided massive fiscal stimulus to help stave off even worse declines. The

short term results seem to be moving in the right direction as May jobs

increased by 2.7 million and 4.8 million June, reported this morning. The labor

participation rate also rose from 60.8% to 61.5% in June. There is a concerning

cliff in front of us as the excess unemployment benefits expire at the end of July

and many states, such as our own, are making decisions to reduce the number of

businesses being opened. While there is ample evidence that the five weeks of protests

have an strong correlation to the location of viral hot-spots, government

officials are still focused on restricting access to small businesses, outdoor

celebrations that are not protests, and backyard BBQs. It seems that until

officials choose to be intellectually honest that either ALL outdoor activities

are a risk or NONE are a risk of viral transmission, people will ignore guidance

because of the obvious contradictions and this virus will continue to vex us

for an extended length of time.

The strong second quarter in the market, following a weak

first quarter, is not without precedence. According to the table below, after a

15% or greater quarterly decline the market rises 70% of the time the following

quarter. While the most recent 19.9% market return was not the biggest in history,

you can see it was the biggest bounce in a quarter since 1938.

Although valuation is a terrible timing tool, especially

during economic or market inflection points, it is always a standard

conversation that needs to be addressed. In the table below you will note that earnings

estimates are declining as the economic slowdown continues (top panel). Given

that stocks have rallied, valuations have risen (bottom panel). Note that this

chart is relatively short term, since 2008, thus it makes the valuation jump

look a bit extreme. If we were to consider the CAPE or other long-term

valuation measures, the market does not look as overvalued. Once again, valuation is a terrible timing

tool for markets because it does not consider the direction of the economy, investor

sentiment, fiscal and monetary policy, nor rates. I do not want to suggest

valuation Is irrelevant, but today valuation is subservient to other factors.

Over the past decade we have witnessed enormous capital

flowing into private equity. It is no secret that many managers have migrated

from making money for their investors to fee generating machines benefiting the

manager. As the past decade progressed, much has been made about the “dry

powder” or available capital to PE firms to take advantage of a market

dislocation. What we are observing is

that many of the larger fund managers with older vintages of funds are stepping

in to help their existing portfolio companies with that dry powder. Newer

managers and/or those without large legacy portfolios are well-positioned to

take advantage of the developing opportunity set. As in most areas of

investing, each manager is unique and over the next two-three years we should

experience a large differentiation in performance between the managers. After extensive

conversations with all of our managers, we feel that the bulk of the portfolio

is in excellent shape to take advantage of this economic environment.

Education has been in the news lately. Will schools open? Is the rapidly rising tuition

worthwhile? Does the brand of school matter?

Strategas group recently analyzed the academic credentials of Chief

Executive Officers of the Fortune 500 companies. Of the five-hundred, 23 had no college degree, thirteen were from the University of Wisconsin System, ten from Harvard, eight from West Point/Penn/Texas A&M, seven from Purdue, and six from Cornell/Iowa State/Michigan/Stanford.

Among the 500, 110 held masters, 29 JDs and 15 PhDs. It appears that if you

want to be a CEO, a degree is required, but there really is no advantage between

schools. Personal qualities and skills matter more, supporting the meritocracy inherent

in the capitalist system. In a nod to a friend, I’m still searching for the CEO

from Cal State LA.

Have a wonderful Independence Day.

Ned